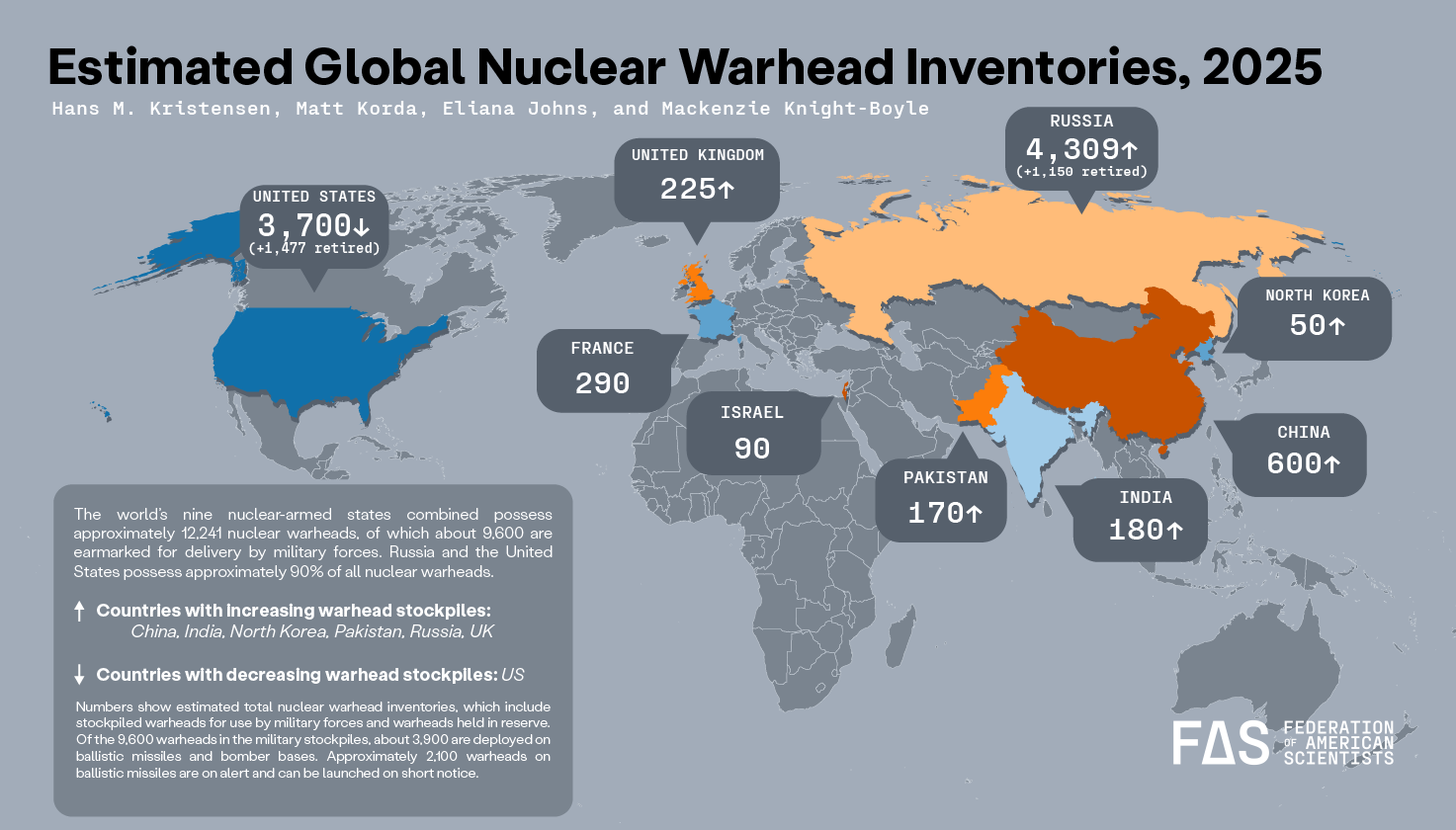

While the Cold War may be a thing of the past, it doesn’t mean the world is less dangerous than it was back then.

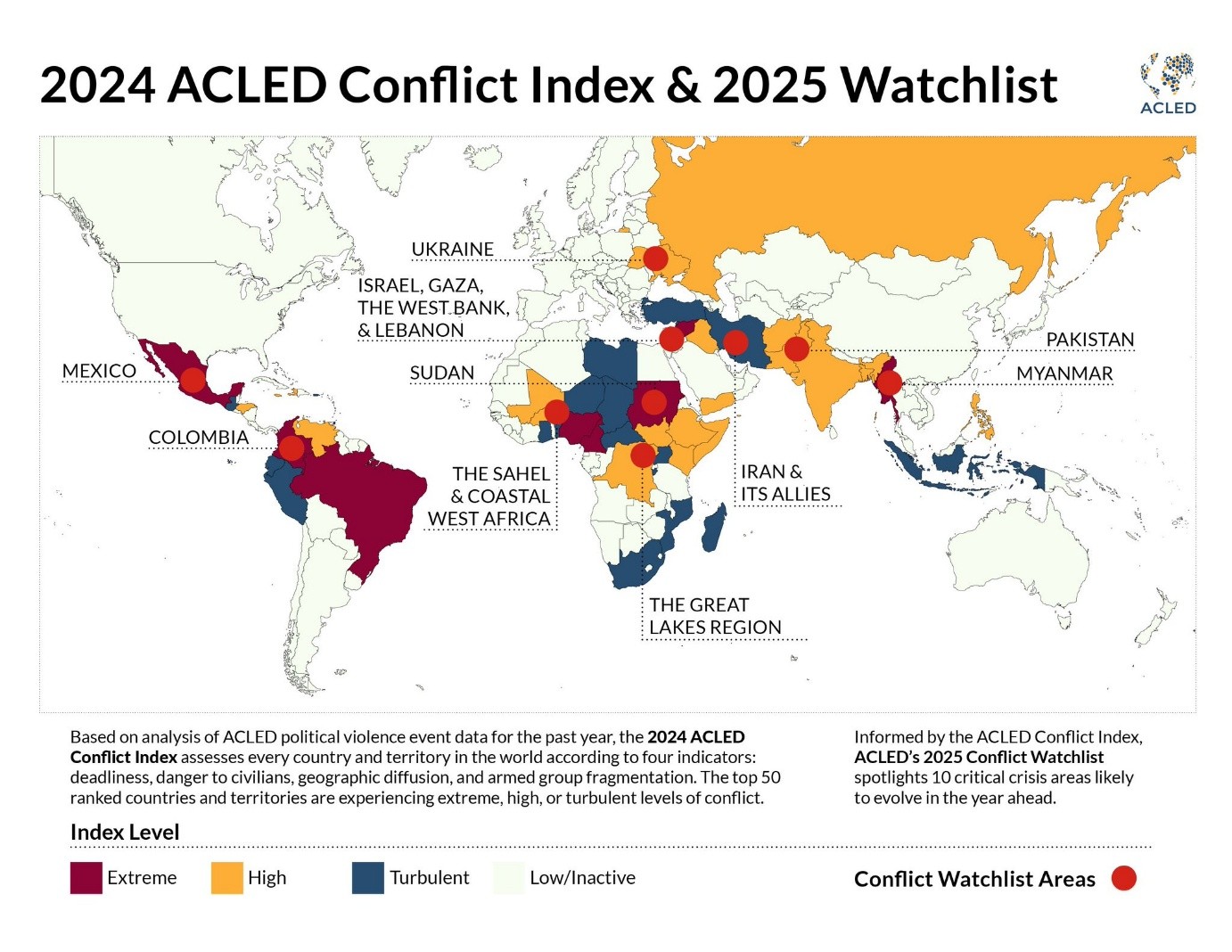

As a matter of fact, the nuclear threat has expanded significantly, and regional conflicts are more prevalent than ever.

What’s more, with US stepping back on its traditional alliances with democratic nations around the world, it has opened up new dynamics and geopolitical risks and opportunities.

For example, the NATO alliance is shifting from a US-led coalition of European nations to a Europe-first footing in coming years.

That has led to massive spending for European defense stocks.

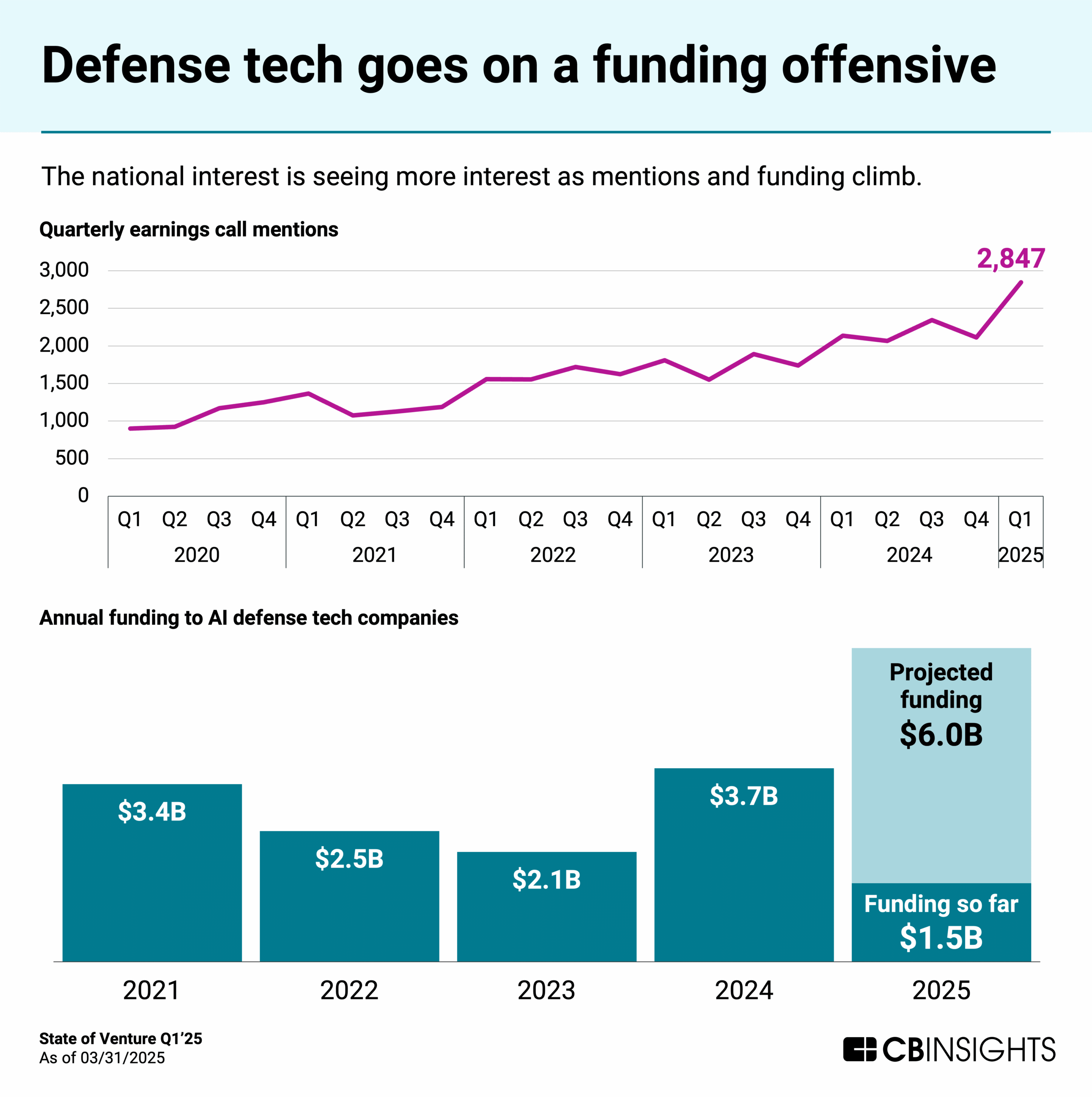

In the US, there’s a major reshuffling of spending and acquisition of new defense equipment, driven largely by the tech sector.

Many tech companies avoided the defense sector, but now as drones, space, and automation have been embraced in the next phase of warfare, they’re stepping in.

It also helps that defense spending is big and reliable – far more reliable than PE or VC funding.

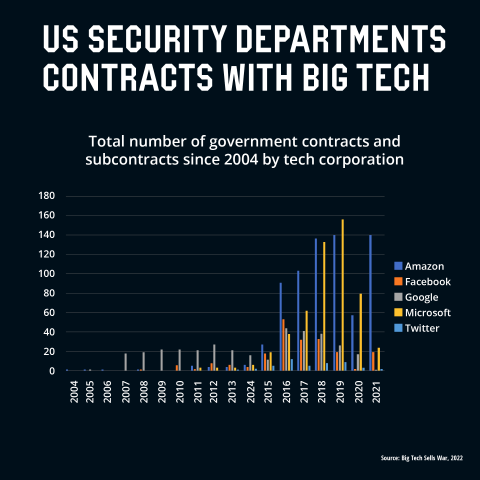

In the US, there’s also a shift from the traditional “primes” (the big prime contractors) that have dominated the defense sector for decades, like Lockheed Martin (NYSE: LMT), RTX (NYSE: RTX), Northrop Grumman (NYSE: NOC), and Boeing (NYSE: BA), to big tech firms like Amazon (NASDAQ: AMZN), Alphabet (NASDAQ: GOOGL), Microsoft (NASDAQ: MSFT), and Meta (NASDAQ: META).

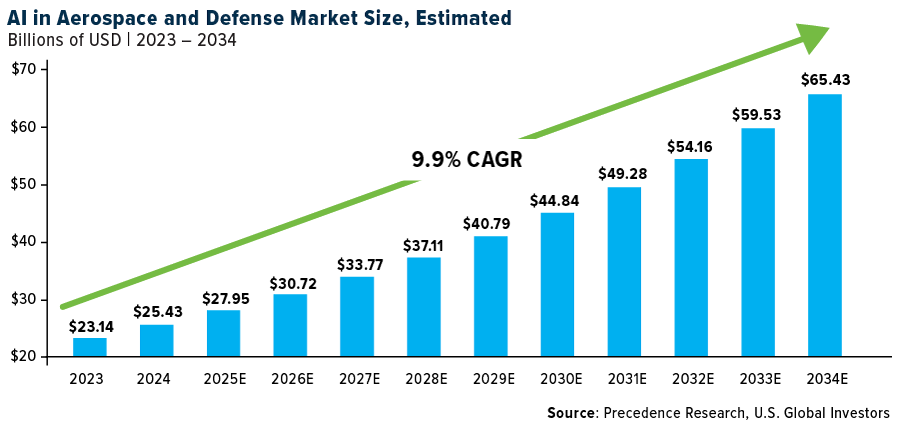

With AI coming on the scene, this kind of Defense 2.0 spending is only going to increase.

What’s more, these numbers don’t even consider the massive spending that is going on in space.

Much of the new defense infrastructure is being built in orbit these days.

This isn’t your grandfather’s space race. Space Race 2.0 has far more participants and it’s not a docile environment.

In coming weeks, we’ll explore specific sectors and how tech is changing the defense game.